Market Commentary – Feb 2020

Derwood S. Chase, Jr., Founder & Chairman Emeritus, Chase Investment Counsel, Market Commentary

Chase Investment Counsel Corporation uses a “bottom up” investment process combining fundamental analysis (the what) and technical indicators (the when) in making judgements about both market timing and stock selection. We focus on mitigating risk.

No one knows how long and how serious the coronavirus will prove to be. The most comparable health scare was the SARS virus in 2002-2003. That involved a significant decline followed by a complete recovery. If the coronavirus is going to be much worse, we should know by the end of February. We have one source that believes the Chinese authorities are still grossly under reporting the numbers, and because China and other poorer Asian countries have inadequate health facilities to handle a massive pandemic the numbers will ultimately be much higher than the stock market is anticipating. China is very important to world trade. A lengthy lock down will affect the demand for oil and many other commodities and disrupt numerous

U.S. firms that rely on China for critical components. However, if the virus does significantly impact our economy, the Federal Reserve will likely reduce interest rates further. Meanwhile with 64% of S&P 500 Index companies reporting 4Q earnings, the blended earnings growth rate is +0.7%, significantly better than the December 31st 4Q estimates of –1.7% for the whole S&P 500. With Asian stock markets at much greater risk than ours, the U.S. may still be the most attractive place to invest. February is the weakest month in the seasonally favorable November-April six months so a short-term correction would be normal.

Many presumed negative economic factors simply don’t correlate with equity prices. For instance, while consumer debt is at a record peak, with lower interest rates and higher consumer income, the payments to service consumer debt as a percent of disposable income has actually declined from 13% in 2008 to less than 10%, close to the lowest level since 1980. Similarly, the U.S. Manufacturing Purchasing Managers Index fell below 48 in December, the lowest in a decade, but as Stansberry’s True Wealth Systems documents, going back 60 years similar instances have led to outperformance by the S&P 500. Subsequently, 6- and 12-month returns were 6.9% and 12.7% respectively compared to all other periods which averaged only 3.5% and 7.0%.

Since stock prices are determined by the forces of Supply and Demand, we pay particular attention to Lowry’s Primary Trend Perspectives research, particularly their Operating Companies Only (OCO) indexes, which eliminates distortions by excluding preferred stocks and ADRs. At the February 6th recovery highs both the NYSE All-Issues and the OCO Advance-Decline Lines failed to confirm the new high of the S&P 500. The divergences were minor. The Large Cap OCO Advance-Decline Line actually confirmed that new high while both the OCO Mid and Small Cap indexes failed to do so while the S&P 400 Mid-Cap Index and the S&P 600 Small Cap Index Relative Strength Lines versus the S&P 500 remained in their long-term downtrends. Lowry’s short-term Supply and Demand figures reversed to a short-term Sell signal by February 7th, but longer term still support a healthy major uptrend.

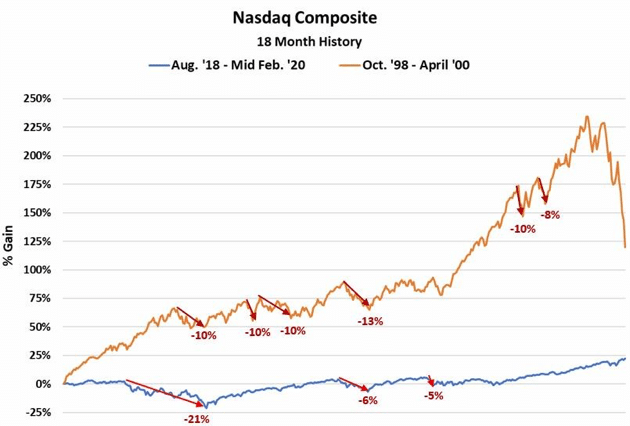

The adjacent chart compares the last 18 months of a typical major bull market (orange line) with the latest 18 months (blue line). We expect this bull market will continue its “melt up” similar to most others. In fact, Nasdaq tech stocks have definitely started. We believe large good quality Growth stocks, as opposed to Value stocks, offer the most potential. Large tech-oriented companies in Artificial Intelligence (AI) sectors as well as information and communication services, payment processing, health services and defense sectors should be among the best performers. Companies that cater to consumers, have high profit margins and require little need for additional investment capital to grow rapidly, should continue to offer the best returns, especially those with substantial trading liquidity to accommodate huge institutional momentum investors.

The adjacent chart compares the last 18 months of a typical major bull market (orange line) with the latest 18 months (blue line). We expect this bull market will continue its “melt up” similar to most others. In fact, Nasdaq tech stocks have definitely started. We believe large good quality Growth stocks, as opposed to Value stocks, offer the most potential. Large tech-oriented companies in Artificial Intelligence (AI) sectors as well as information and communication services, payment processing, health services and defense sectors should be among the best performers. Companies that cater to consumers, have high profit margins and require little need for additional investment capital to grow rapidly, should continue to offer the best returns, especially those with substantial trading liquidity to accommodate huge institutional momentum investors.

Chase Investment Counsel Corporation is the oldest independent investment counsel firm domiciled in Virginia. We’re not in the brokerage business, but act as portfolio managers and purchasing agents for our clients. As Barron’s described us in 1972, we’re located “Far from the Madding Crowd” in Charlottesville, Va. Besides Derwood Chase, we have an excellent “next generation” group of officers that average 49 years of age and over 18 years of experience. Three of our officers have MBAs, one is a CFA and two are CMTs. We recognize that markets are driven by company fundamentals as well as technical factors which reflect investor sentiment.

In addition to our own research, and that from several brokerage firms, we utilize over 40 independent research sources selected with the benefit of over 50 years experience. Our investment process was developed over more than 50 years and is rather unique in combining fundamental and technical analysis to mitigate risk and build diversified, high quality, reasonably priced growth oriented portfolios. We manage large, mid-cap, and all-cap equity oriented portfolios as well as balanced funds for individuals and trust clients (minimum normally $1 million) in 15 states. We also indirectly serve about 2,000 investors through our mutual fund product. As a smaller firm, we have a particular advantage in managing portfolios since we don’t need huge marketability to acquire or eliminate stock positions promptly without significantly affecting the market. We are not in the brokerage or banking business and do not have the conflicts of interest and the other priorities those businesses involve.