A Second Lockdown of the Economy?

Derwood S. Chase, Jr., Founder & Chairman Emeritus, Chase Investment Counsel, Market Commentary

Chase Investment Counsel Corporation uses a “bottom up” investment process combining fundamental analysis (the what) and technical indicators (the when) in making judgements about both market timing and stock selection. We focus on mitigating risk.

The most worrisome market negative continues to be COVID-19 and a possible second lockdown of the economy. We expect it to take many years (the Congressional Budget Office estimates 2028) before our economy gets back to 2019 levels. Even then, corporate profit margins may not be as high, especially if corporate taxes are raised. The Fed recently announced that it will keep yields near zero through 2022. It has also prohibited banks from repurchasing shares and increasing dividends in view of the potential for higher losses on non-performing loans.

Markets seem quite willing to look past the depressed economy as the second quarter rise of 20% by the S&P 500 Index shows. The stock market pattern of higher highs and higher lows with the underlying forces of Supply and Demand, market breadth, participation and momentum are all consistent with a healthy and sustainable intermediate-term uptrend. Lowry’s Research points out that by May 28th the percent of NYSE Issues above their 10-week Moving Average rose to over 90%, an infrequent “overbought” level, which in the last 30 years has been followed by average 12 month S&P 500 returns of 16%. Even if we use 2022 S&P 500 estimates the P/E multiple is still over the 5 and 10-year average P/E multiples of 16.9 and 15.2, respectively. However, on a relative value basis with competing alternative investments such as the 10 Year U.S. Treasury bonds, which yield less than 0.7%, stocks seem relatively attractive. The Fed is determined to head off a pandemic induced depression by using 10x more monetary stimulus than during any prior economic crisis. Congress has also approved trillions of dollars of fiscal stimulus. Many investors are currently bearish and both the S&P and Nasdaq short positions are the highest since 2011. The demand from presently short investors as well as from other investors with trillions of dollars on the sidelines means any near term market correction is likely to be modest. With intermediate market indicators favoring a continuation of the rise despite the headwinds of economic stagnation we could experience a long-term range bound market similar to the ones we experienced between 1999 and early 2002 and 1966 to 1975.

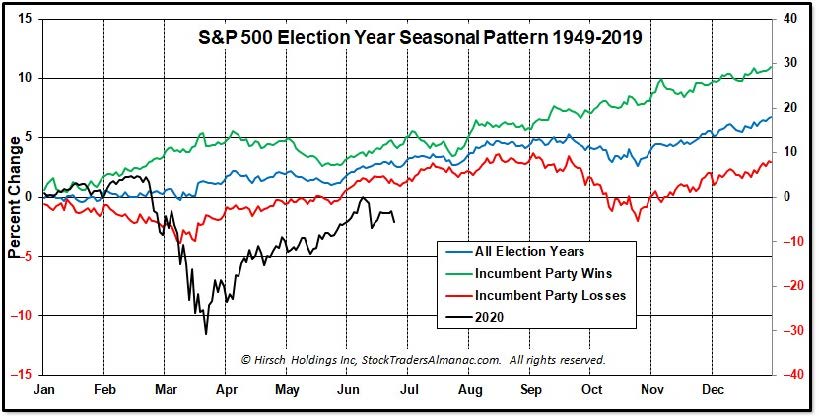

Clearly stock market gains have mostly been the result of excess liquidity, not a return to good economic conditions. As you can see from the presidential election year chart patterns of 1949-2019, there is approximately a 25% difference in the S&P 500 performance between election years when a sitting president is running for reelection and his party wins

Clearly stock market gains have mostly been the result of excess liquidity, not a return to good economic conditions. As you can see from the presidential election year chart patterns of 1949-2019, there is approximately a 25% difference in the S&P 500 performance between election years when a sitting president is running for reelection and his party wins

and the years when it loses. So far, the 2020 year-to-date performance is tracking the trend of the red incumbent party losses line more closely. It still seems generally prudent to maintain modest cash reserves in our equity portfolios while balanced portfolios are now a little over 60% equities/40% bonds and cash equivalents. We have been investing in many companies which are able to continue their good growth even in a stay-at-home environment. Those companies are popular and quite fully priced now which means they are also vulnerable to any unexpected market decline.

With a great deal of criticism and pessimism in the U.S. at this time, we thought investors might want some historical perspective. The U.S. share of the world GDP stood at 25% in 1980 and after some faltering during subsequent decades, by 2020 it had bounced back to 25% again. During that same 40 years, the European Union fell from 35% of world GDP to 25%. Japan’s share slipped from 10% to 6%, while Russia dropped from 3% to 2%. Meanwhile, China, with its 1.4 billion people, rose from 2% to 16%. The U.S. stock market rose by 250% in the past decade and accounted for 56% of the global stock market capitalization by 2020 up from 42% in 2010, while China’s stock market rose just 70%.

Chase Investment Counsel Corporation is the oldest independent investment counsel firm domiciled in Virginia. We’re not in the brokerage business, but act as portfolio managers and purchasing agents for our clients. As Barron’s described us in 1972, we’re located “Far from the Madding Crowd” in Charlottesville, Va. Besides Derwood Chase, we have an excellent “next generation” group of officers that average 49 years of age and over 18 years of experience. Three of our officers have MBAs, one is a CFA and two are CMTs. We recognize that markets are driven by company fundamentals as well as technical factors which reflect investor sentiment.

In addition to our own research, and that from several brokerage firms, we utilize over 40 independent research sources selected with the benefit of over 50 years experience. Our investment process was developed over more than 60 years and is rather distinct in combining fundamental and technical analysis to mitigate risk and build diversified, high quality, reasonably priced growth oriented portfolios. We manage large, mid-cap, and all-cap equity oriented portfolios as well as balanced funds for individuals and trust clients (minimum normally $1 million) in 11 states. We also indirectly serve about 2,000 investors through our mutual fund product. As a smaller firm, we have a particular advantage in managing portfolios since we don’t need huge marketability to acquire or eliminate stock positions promptly without significantly affecting the market. We are not in the brokerage or banking business and do not have the conflicts of interest and the other priorities those businesses involve.